Billethead

7 Juillet 2020

Since in many cases US investors are not subject to state income taxes and, therefore, the effective tax paid in the US is not above the 75% threshold, PTR rules should be carefully observed for US residents intending to apply the 35% net gain alternative when selling equity participations in Mexican companies.To that end, investors that engage in share-purchase transactions that are taxable in Mexico should carefully review the facts and circumstances surrounding them to avoid any potential or unnecessary tax contingencies. All.PTR rules were included in the Mexican Income Tax Law as of 1997.As of today, PTR rules generally seek to levy income derived by Mexican residents through foreign entities or legal vehicles in which they participate, directly or indirectly, prior to such Mexican residents effectively obtaining the income. EN SAVOIR PLUS >>>

Image source: www.captaineconomics.fr

Originally a criteria set out in the harmful tax framework from 1998, it had not been applied to date.Finally it contains next steps for the work on harmful tax.One part relates to preferential tax regimes, where a peer review is undertaken to identify features of such regimes that can facilitate base erosion and profit shifting, and therefore have the potential to unfairly impact the tax base of other jurisdictions.One part of the Action 5 minimum standard relates.The second part includes a commitment to transparency through the compulsory spontaneous exchange of relevant information on taxpayer-specific rulings which, in the absence of such information exchange, could give rise to BEPS concerns.This report includes two important annexes.Since the start of the BEPS Project, the FHTP has reviewed almost 290 preferential tax regimes.Please upgrade your browser to improve your experience.The Inclusive Framework on BEPS has decided to resume the application of the substantial activities requirement for no or only nominal tax jurisdictions.

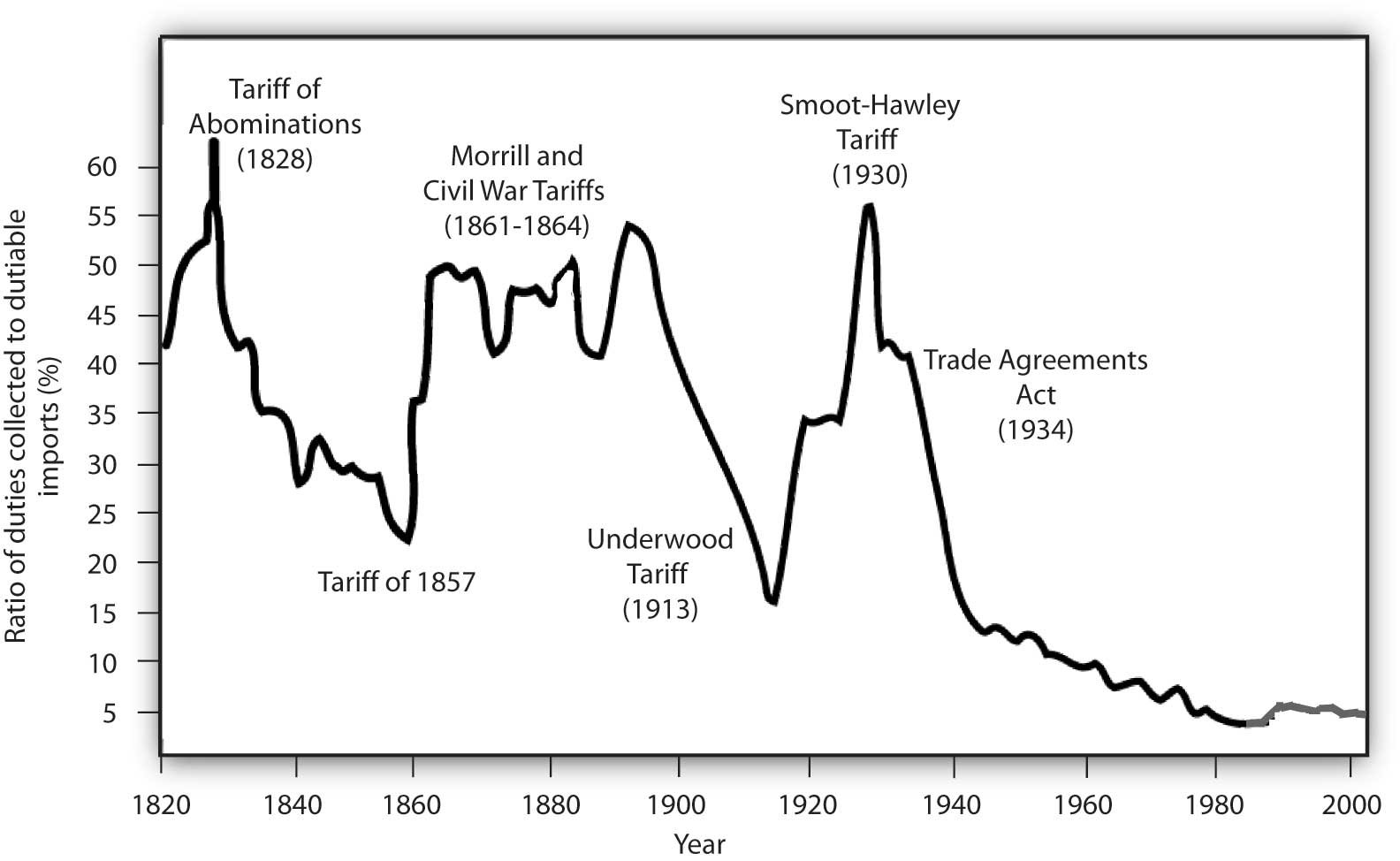

Image source: www.bac-s.net

This progress report is an update to the 2015 BEPS Action 5 report and the 2017 Progress Report. Finally it contains next steps for the work on harmful tax practices. This report includes the details of this new standard and the other work on additions to and revisions of the harmful tax practices framework.BEPS Action 5 is one of the four BEPS minimum standards which all Inclusive Framework members have committed to implement. It contains the results of review of all BEPS Inclusive Framework members’ preferential tax regimes that have been identified since the BEPS Project. One part of the Action 5 minimum standard relates to preferential tax regimes where a peer review is undertaken to identify features of such regimes that can facilitate base erosion and profit shifting, and therefore have the potential to unfairly impact the tax base of other jurisdictions.

By using Orbitax's services, you agree that we may store cookies on your device.Lucia, Seychelles, Turks and Caicos, United Arab Emirates, US Virgin Islands, Vanuatu, and Wyoming (US); and Harmful Tax Practices.

The Case of European Patent Boxes, CESifo Working Paper No., Liberini, F.It will be treated confidentially and will not be handed on to third parties., and M.You can unsubscribe at any time via the links given in our emails. The estimate is in line with estimates reported in recent studies on profit shifting, where the consensus estimate is 0. Details.This manifests in the rapid growth of the digital economy that has evoked an intensified interest?on the part of the EU and its member countries not only to foster technological innovations, but also to compete for innovative, internationally mobile firms. Stimmelmayr (2018), Is it just Luring Reported Profits.Against this background, the question arises to which extent patent boxes facilitate profit shifting of MNEs and whether countries with a patent box indeed benefit from the associated profit shifting behaviour of MNEs. US tax reform and German license barrier rules.

56765.56.34.99

, Schwarz, 2011, and Keen and Konrad, 2013 ).I f countrie s wer e instea d force d t o trea t al l base s alike, the n th e in - centiv e t o compet e fo r th e mor e mobil e base s woul d intensif y th e tendenc y t o compet e fo r th e les s mobil e base s t o suc h a n exten t tha t th e equilibriu m outcom e coul d be?is, i n th e mode l use d below.g.Nevertheless, th e presen t analysi s sug - gest s quit e strongl y tha t th e debat e o n harmfu l ta x competitio n ha s neglecte d a po - tentiall y importan t consideration: preferen - tia l regime s ma y serv e a usefu l purpos e i n limitin g th e scop e o f ta x competition, an d prohibitin g the m ma y lea d t o ta x competi - tio n tha t i s les s dramatic, bu t als o mor e pervasiv e an d consequentl y als o mor e harmful.Mos t obviously, b y of - ferin g preferentia l regime s the y ca n com - pet e fo r th e mos t mobil e base s withou t undul y distortin g thei r taxatio n o f les s mobil e ones. MOF publishes list of preferential tax regimes for.

Image source: i-df.unimedias.fr

The foreign part of this income, the FDII, is then calculated by multiplying the deemed intangible income by the ratio of foreign income from sales and services to the overall income.To this end, they allow a partial deduction?for FDII when determining the income, resulting in an effective tax rate for this income of 13. 4j ITA obviously breaches constitutional and EU law.125%.Given the wording of the law and the reasoning and history of the license barrier, the authors conclude that the FDII provisions do not constitute a preferential tax regime.Flick Gocke Schaumburg, Taxand Germany, explores.Now the question arises of whether these new provisions constitute a preferential tax regime in the above sense, resulting in a (partial) non-deductibility of license fees paid by German licensees to US licencors.Although it must be expected that the German tax authorities will take a different position on the issue, taxpayers are well advised to take legal measures against potential claims of the

Image source: i-df.unimedias.fr

.

The development and diffusion of new technologies scores high on the policy agenda of the European Union (EU) as well as its member states. The EU seeks to limit the technological gap towards other major economies. This manifests in the rapid growth of the digital economy that has evoked an intensified interest?on the part of the EU and its member countries not only to foster technological innovations, but also to compete for innovative, internationally mobile firms..

PDF | A key feature of the recent EU and OECD standards for good behavior in international taxation is a presumption against preferential tax regimes... | Find, read and cite all the research you need on ResearchGate

/http%3A%2F%2Fwww.ceintureventreplat.fr%2Fimages%2Fperdre-du-poids-doctissimo_7.jpg)

/https%3A%2F%2Fimage.jimcdn.com%2Fapp%2Fcms%2Fimage%2Ftransf%2Fnone%2Fpath%2Fs63ccf77ce0e97436%2Fimage%2Fi6febdcddc34efe74%2Fversion%2F1456254609%2Fimage.jpg)

/https%3A%2F%2F4.bp.blogspot.com%2F-zLbp0OukoNc%2FVFUPU4mk7NI%2FAAAAAAAAB_k%2Fg2fOAT7k8qs%2Fs1600%2Friz%252Bau%252Bpoulet%252Bcourgettes%252Bet%252Bpoivrons.jpg)

/https%3A%2F%2Farchzine.fr%2Fwp-content%2Fuploads%2F2017%2F04%2Ftresse-cheveux-style-sir%25C3%25A8ne-comment-faire-une-tresse-un-mod%25C3%25A8le-de-natte-f%25C3%25A9minin-moderne-et-%25C3%25A9l%25C3%25A9gant-e1491307533947.jpg)